The credit to the rent revenue account increases the revenue account, as the company has earned the rent payment. Recent updates to lease accounting, including new standards ASC 842, IFRS 16, GASB 87, and SFFAS 54, have changed the accounting treatment for some types of leasing arrangements. In short, organizations will now have to record both an asset and a liability for their operating leases.

Gross Method Accounting: Principles, Impact, and Comparisons

Another important ratio influenced by rent receivables is the days sales outstanding (DSO). This metric calculates the average number of days it takes to collect rent after it has been invoiced. A lower DSO suggests that the company is quick in converting receivables into cash, which is beneficial for maintaining liquidity.

Capital/Finance Lease vs. Operating Lease Explained: Differences, Accounting, & More

Now that we have all the inputs ready, we can move on to the core step of recording the rent receivable transaction. Rent received in advance is shown rent receivable journal entry under current liability in the balance sheet. Entities paying GST have to charge GST on the rental services provided by them to the tenants.

Accrued Rent Receivable

Each type of rent may have different recognition criteria and may need to be recorded separately to provide a clear and comprehensive view of the financial obligations and entitlements. If the lease payment is variable the lessee cannot estimate a probable payment amount until the payment is unavoidable. Even if a high certainty the performance or usage the variable lease payment is based on will be achieved does exist, the payments are not included in the lease liability measurement. While it is highly probable performance or usage will occur, neither of these things are unavoidable by the lessee until after they have been completed.

To summarize, rent is paid to a third party for the right to use their owned asset. Renting and leasing agreements have existed for a long time and will continue to exist for individuals and businesses. With the transition to ASC 842 under US GAAP, some of the terminology and accounting treatments related to rent expense are changing. Generally, variable, or contingent rent, is expensed as incurred according to both legacy accounting and the new accounting standard.

- Under ASC 842 periodic lease expense is made up of the periodic interest and asset depreciation shown in columns “liability lease expense” and “asset lease expense,” respectively.

- This was beneficial to lessees in that the obligation for those payments did not drive up the liability balance.

- A landlord could offset this receivable with an allowance for doubtful accounts, if there is a probability that a tenant will not pay rent.

- The credit side of the entry at the end of the first year will include the cash paid for the first year of $100,000.

- Moreover, the balance sheet will report the total balance of the outstanding rent receivables account as of the close of the fiscal year as a company asset.

Per ASC 842, the ROU asset is equal to the lease liability calculated in step 3 above, adjusted by deferred or prepaid rent and lease incentives. In this example, it is the liability of $11,254,351 minus the incentive balance of $200,000. The lease term is 120 months (from step 1) and total rent is $15,767,592 (from step 1). Straight-line monthly rent expense calculated from base rent is therefore $131,397 ($15,767,592 divided by 120 months).

Lease payments decrease the lease liability and accrued interest of the lease liability. A lease expense, equivalent to the straight-line rent expense recognized under ASC 840 for operating leases, is recognized for interest accrued on the lease liability and amortization of the ROU asset. Deferred rent is primarily linked to accounting for operating leases under ASC 840. Nevertheless, differences between lease expense and lease payments also exist under ASC 842.

The recognition of rent receivable begins with the establishment of these contracts, which serve as the primary source of information for recording transactions. The clarity and specificity of lease agreements are paramount, as they directly influence the accuracy of financial records. In the case of a rent accrual, the company records the rent expense but the payment is not yet due. In this case, at the period adjusting entry of January 31, 2021, the company ABC needs to make the journal entry for accrued rent revenue that it has earned in January 2021 for the office space rental fee. The total lease expense of $115,639 is recognized at the end of the first year.

Here is the journal entry at transition – showing the debit to accrued rent to remove the balance from a separate account and credit to the ROU asset to adjust the beginning balance. Under ASC 840, a rent accrual liability was recorded in periods when rent was incurred, because the company used or occupied the leased asset and not yet made a payment. The entity received the economic benefit of the leased asset in the period and has an obligation to pay for the benefit it received. Accrued rent receivable is the amount of rent that a landlord has earned, but for which payment from the tenant is still outstanding.

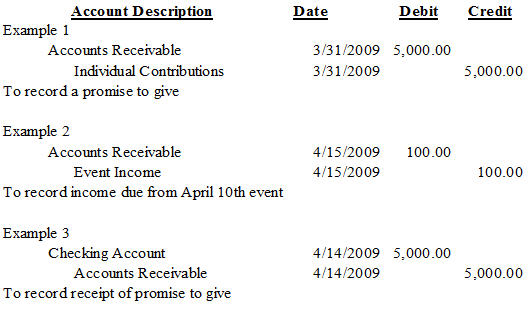

The journal entry is also used to record the exchange of goods or services for the rent payment. For example, if the customer is paying rent for the use of a space, the journal entry will record the rental payment and the space that the customer is using. This helps to ensure that the company is accurately tracking its income and expenses. When the tenant makes a payment, the landlord reverses the journal entry and credits the Cash account and debits the Rent Receivable account. Rent receivable is an asset account that represents rent that has been earned but not yet collected.